Nikkei Real Estate Market recorded 288 cases of sales during the

period from January through March 2010, representing a year on-

year gain of 13% and a sign that the market is recovering. The

demand is being pulled by major J-REITs that have switched to

the offensive with the improved capital raising environment. The

REITs are in fact rebuilding their portfolios, with their more than

150 billion yen [$1.6 billion] in acquisitions offset by 90 billion

yen [$960 million] in sales. The residential market is seeing more

transaction activity, including condominium sites and mid-development

projects.

The trend of a recovery in the REIT market has

become clear with the improvement in the capital

raising environment. Figure 1 shows the history of

transaction amounts for REITs by quarter, and the

trend of capital raising through REIT public offerings

by quarter is indicated in Figure 2. There were 34

acquisitions between January and March 2010 for a

total of 159.1 billion yen [$1.7 billion]. Although this

is far less than previous levels, it is the second straight

quarter following the period from October through

December 2009 in which 150 billion yen [$1.6 billion]

has been exceeded. Although the deal is not shown in

the figure, in April Mori Trust Sogo REIT acquired

50% joint ownership in the Tokyo Shiodome Building

{kind=link}

for 110 billion yen [$1.2 billion].

An analysis of the capital raising conditions of REITs

shows that there have been repeated capital raisings

since November 2009, when a public offering was

conducted for the first time in 15 months. Most of

the capital that has been raised has been applied to

the acquisition of properties. January 2010 saw the

first issuance of investment corporation bonds in a

public offering in 20 months. The first, conducted by

Nippon Building Fund, raised 10 billion yen [$110

million] and was followed by four other REITs.

While there have been repeated acquisitions of largescale

properties, another feature of recent REITs is that

there has also been an increase in sales. In the January

to March 2010 period, there has been 91.2 billion yen

[$970 million] in sales. These include such REITs as

Invincible REIT, which sold 46 properties including

Growth Maison Ginza over several deals to raise 27.3

billion yen [$290 million] as a means to suppress

interest-bearing debt. However, there are also more

cases of REITs rebuilding their portfolios through

dynamic sales and acquisitions of assets. Japan

Retail Fund sold Urawa Parco for 26.1 billion

yen [$280 million] and used that money to acquire

seven properties in Tokyo and Osaka consisting of

retail facilities and plots of leased land under the

facilities. Their acquisitions totaled

approximately 24.4 billion yen

[$260 million]. ORIX JREIT

sold two office buildings in Tokyo

for a total of 13.1 billion yen [$140

million] and acquired six properties

consisting of logistics facilities and

retail buildings for a total of 31.5

billion yen [$340 million].

An analysis of the entire market

including non-REIT transactions

reveals that the number of deals

posted a year-on-year increase

following the October to December

2009 quarter. Figure 3 shows a

history of deals by property type

through year-on-year comparisons.

Hous i n g r ebounded f r o m i t s

preceding drastic slump to increase

by 153% and post deals roughly 2.5

times that of the same period a year

earlier.

F igu r e 4 i s a l i s t o f m a j o r

transactions during the period.

Of the transactions for which the

prices are known, there were 12

transactions worth at least 10 billion

yen [$110 million] including bulk

sales. The most expensive property

was the former Mitsukoshi Ikebukuro

store, whose sale agreement was

concluded in September 2008 and

which was sold in January 2010

with all cash provided by home

appliance retailer Yamada Denki.

The second largest transaction was

the 45 billion yen [$480 million]

acquisition of the Aoyama Building

by a fund of Mitsubishi Jisho

Investment Advisors. The seller

was Mitsubishi Estate, which

registered a valuation loss on its

equity investments of 54.4 billion yen

[$580 million] due to the impairment

loss of Tokyo development sites and

other reasons in its settlement for the

March 2010 period. Nevertheless,

the company secured a profit for the

year by generating 22.9 billion yen

[$240 million] in profit through this deal. Nippon Oil bought 27% of the interest in the

Resona Maruha Building from Mitsubishi Estate for

42 billion yen [$450 million] and simultaneously sold

11.64% of the interest in GranTokyo South Tower for

40 billion yen [$430 million].

Figure 5 below takes the office buildings sold during

this quarter and the previous quarter for which the

price is known and indicates the sales price per square

meter of rentable floor space (unit price per square

meter). Figure 6 indicates the distribution of cap rates

estimated based on new closing rents and vacancies

using the weighted average by area.

In this case, the average unit price per square meter

for the five central wards of Tokyo is 1.95 million

yen [$21,000] and the cap rate is 3.7%. The average

unit price per m2 for Chiyoda Ward is high at 2.69

million yen [$29,000] and the cap rate is low at 3.2%.

These numbers were impacted by two large deals:

GranTokyo South Tower and the Resona Maruha

Building. An analysis of the cap rate distribution

shows that there are many cases in Chiyoda Ward and

Minato Ward where the cap rates are on the 3% to 4%

level and that the cases in Shinjuku Ward and Shibuya

Ward often surpass 5%.

Further, note that there are cases where the cap rates

differ from the actual returns since the cap rates

assume that vacant buildings are filled by tenants and view all buildings as solely office buildings, even when

a building contains retail stores and/or residential

floors.

Price of Ark Mori Building drops by 40%

Figure 7 indicates the cap rate of office buildings

transacted during this period in ascending order by

cap rate. Clearly, the highest unit price per square

meter was the 4.31 million yen [$46,000] registered

with the GranTokyo South Tower and the lowest cap

rate was 2.5% for the same transaction.

The next lowest cap rate was the Roppongi Hills

Mori Tower transaction in which Mori Hills REIT

acquired a portion of the tower from its sponsor

Mori Building. After the acquisition, Mori Hills

REIT is leasing the property to Mori Building at

a fixed rent. The cap rate calculated based on the

disclosed rental income is 4.1% but according to

our calculations, which take into consideration the

high vacancy rate in the area, the cap rate is 2.6%.

Similarly, the Ark Mori Building acquired by the

same REIT had a unit price per square meter of 2.43

million yen [$26,000]. The REIT also acquired part

of the same building in March and September 2008

and the respective unit prices per square meter at

those times were 4.15 million yen [$44,000] and 4.21

million yen [$45,000], respectively. This means that

the unit price in the past two years fell by around

40%.

In areas other than the Tokyo metropolitan area,

the number of overall deals remains low and office

buildings transactions are rare. The JPR Nagoya

Sakae Building and NBF Hakata Gion Building were

both sold as a part of the process of REITs rebuilding

their portfolios. The price of the NBF Hakata Gion

Building fell by 16% compared to its acquisition in

2001. In Osaka City, the former Access Headquarters

Building and one other building sold for about 7

billion yen [$75 million], 30% of the price three years

ago.

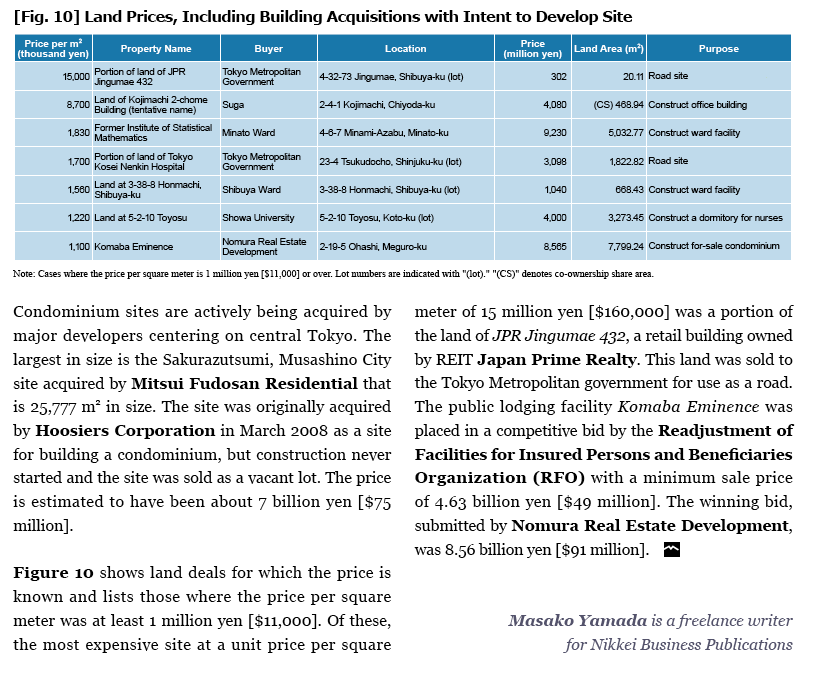

In accordance with the increase in residential

transactions, the acquisition of condominium sites

particularly stood out during this period. Among

the noteworthy cases are the acquisition of entire

the number of overall deals remains low and office

buildings transactions are rare. The JPR Nagoya

Sakae Building and NBF Hakata Gion Building were

both sold as a part of the process of REITs rebuilding

their portfolios. The price of the NBF Hakata Gion

Building fell by 16% compared to its acquisition in

2001. In Osaka City, the former Access Headquarters

Building and one other building sold for about 7

billion yen [$75 million], 30% of the price three years

ago.

In accordance with the increase in residential

transactions, the acquisition of condominium sites

particularly stood out during this period. Among

the noteworthy cases are the acquisition of entire

buildings in in-process developments as well as

finished rental condominiums and conversion of them

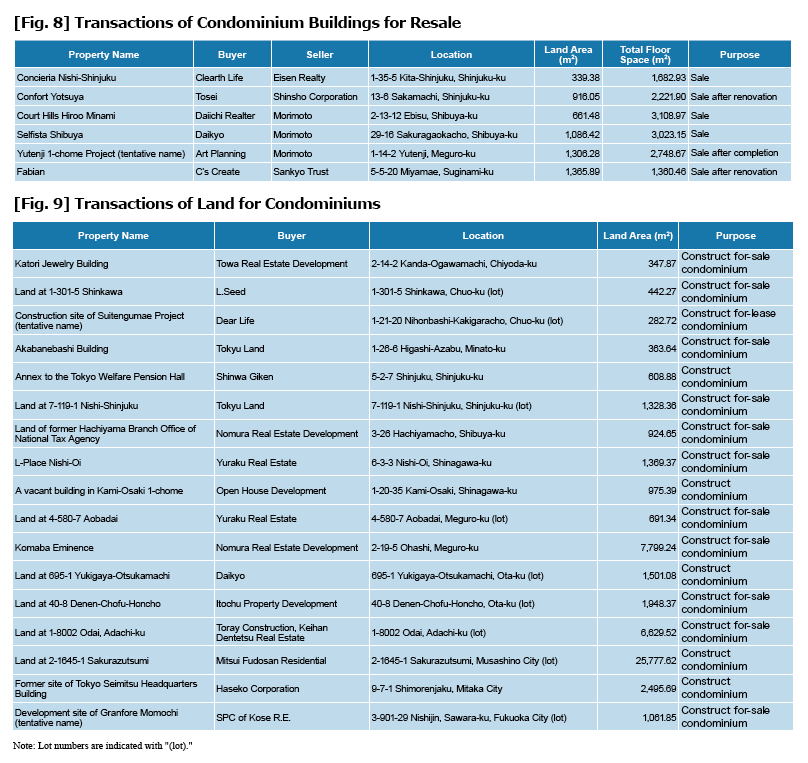

into for-sale condominiums. Figure 8 shows the

deals for condominiums being subdivided and resold,

and Figure 9 indicates the deals for condominium

sites.

Four condominiums bought to be subdivided and

resold were acquired from the bankrupt Morimoto

and Eisen Realty. The buyers, Clearth Life and

Daiichi Realter, are focusing on this business of

acquiring condominiums whose entire buildings are

sold and subdividing them for resale. Meanwhile,

Confort Yotsuya and Fabian are properties that were

built several years ago. These will be subdivided and

sold after renovations.

finished rental condominiums and conversion of them

into for-sale condominiums. Figure 8 shows the

deals for condominiums being subdivided and resold,

and Figure 9 indicates the deals for condominium

sites.

Four condominiums bought to be subdivided and

resold were acquired from the bankrupt Morimoto

and Eisen Realty. The buyers, Clearth Life and

Daiichi Realter, are focusing on this business of

acquiring condominiums whose entire buildings are

sold and subdividing them for resale. Meanwhile,

Confort Yotsuya and Fabian are properties that were

built several years ago. These will be subdivided and

sold after renovations.

No comments:

Post a Comment